Traders

See surface, skew, flies, and term structure in one live view.

Track BTC and ETH volatility moves without switching between exchange screens, spreadsheets, and model diagnostics.

Audience

Derivasys connects BTC and crypto volatility surface monitoring, options skew, term structure, and SVI model diagnostics without separating the fit from the market state.

Traders

Track BTC and ETH volatility moves without switching between exchange screens, spreadsheets, and model diagnostics.

Quants

Review fitted smiles, tenor structure, quote-through-fit behavior, and surface diagnostics from the same market snapshot.

Developers

Use structured surface, smile, risk-node, and diagnostic outputs for internal tools, alerts, and downstream research.

Product previews

These are the core product views: surface, risk analytics, fitted smiles, skew, flies, and calibration diagnostics. The written explainers stay further down for SEO and deeper reading.

Live monitoring

Derivasys is built around the operational questions that matter during active markets: where the surface sits, what venues are quoting, and whether the fit is ready to trust.

01 / Surface

Monitor BTC and crypto SVI output without separating the model from the live options board.

02 / Market

Bid, ask, trade IV, and fit-through checks sit next to the calibrated surface.

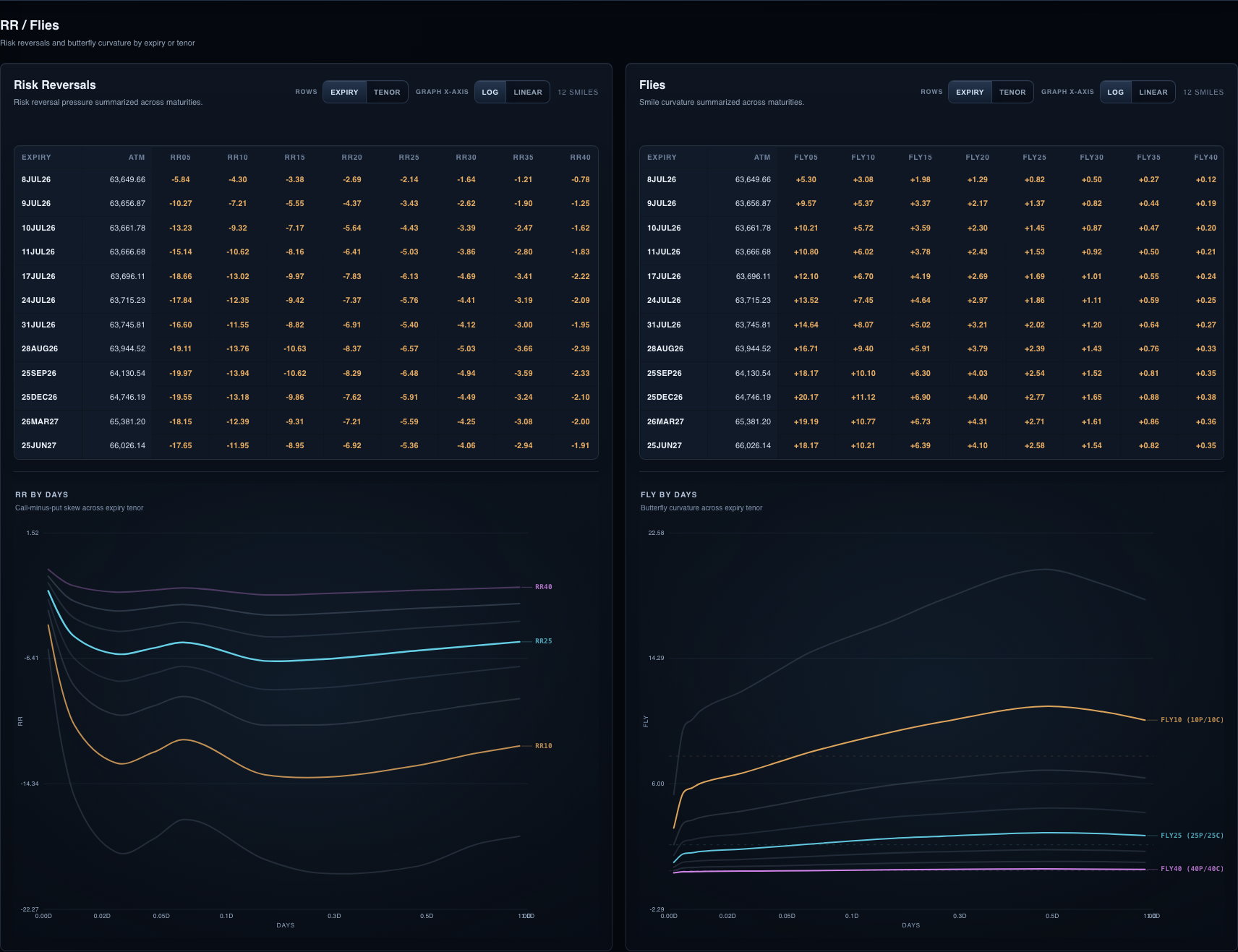

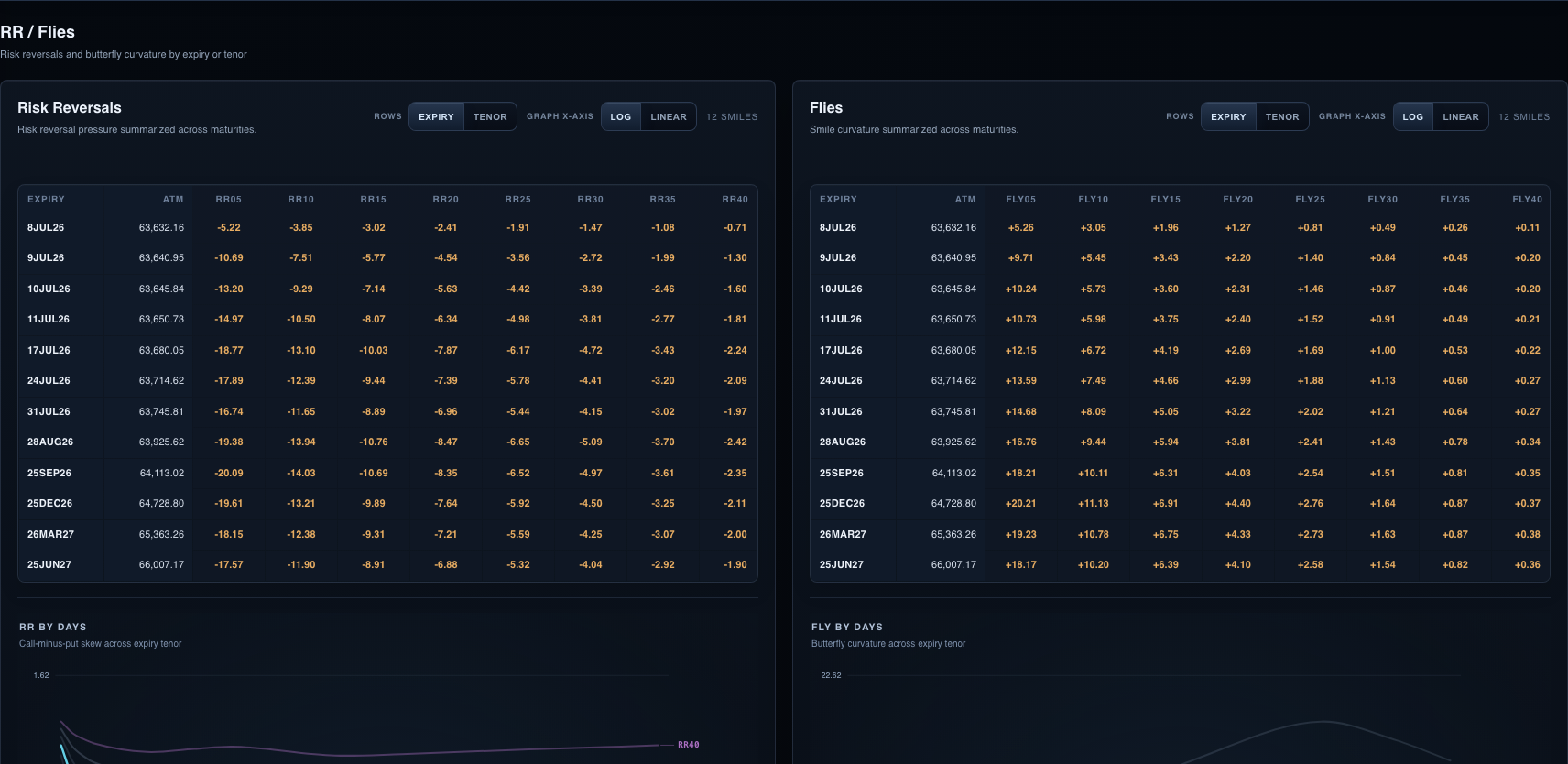

03 / Risk

Read risk reversals, flies, node volatility, and tenor analytics from the same market state.

04 / Diagnostics

Queue state, update timing, fit quality, and quote-through-fit checks make the surface reviewable.

05 / API

Contact us for WebSocket and REST API access to surfaces, smiles, diagnostics, risk nodes, and fixed-tenor views.

Volatility explainers

Use these pages to connect model output, smile shape, and trader-facing risk nodes before inspecting the live dashboard.

Surface

Start with the core concept: smiles connected across expiries into a strike-and-tenor view.

IV

Convert option prices into implied volatility before comparing strikes, expiries, and venues.

Forward

Use total variance across expiries to isolate volatility implied for a future time window.

Variance

Connect realized variance, implied variance, and the option surface behind variance-risk payoffs.

Smile

Read one expiry slice across strikes before it becomes part of the full volatility surface.

SVI

Read the raw SVI formula, parameter meanings, BTC smile example, and production calibration checks.

SSVI

Tie SVI slices together with a surface-level total-variance parameterization and arbitrage checks.

Local vol

Use the Dupire formula to connect a smooth option price surface to model dynamics.

SABR

Understand alpha, beta, rho, vol-of-vol, and how SABR-style smiles compare with SVI.

RR

Use 25-delta call-minus-put volatility to read signed skew across expiries.

Greeks

Connect delta, gamma, vega, and theta to the live volatility surface and risk-node workflow.

Fly

Measure wing richness and smile curvature from same-delta puts, calls, and ATM volatility.

Sticky

Compare listed-strike and delta-bucket conventions when the forward moves.

Market data to dashboard

Normalize exchange quotes, trades, futures, and expiry metadata into clean option inputs.

Calibrate SVI smiles, tenor rows, risk nodes, and surface diagnostics from the latest market state.

Stream compact snapshots and patches into the dashboard and API clients for monitoring.

Engineering notes

Derivasys technical articles document the live BTC options data pipeline, real-time surface construction, order-book handling, SVI fitting, production monitoring, and the Kafka/Kubernetes roadmap behind trader-facing implied volatility analytics.

Series 01

A Derivasys engineering article on building real-time crypto volatility surfaces: live market data, SVI fitting, event-loop pressure, and scaling limits.

Series 02

A Derivasys engineering article on crypto options WebSocket ingestion, order-book construction, real-time implied volatility, SVI fitting, and dashboard state.

Series 03

A Derivasys engineering article on performance tuning implied-volatility calculation, event-loop latency, and selective recalculation for live BTC options surfaces.

Series 04

A Derivasys engineering article on monitoring real-time crypto volatility surfaces: feed freshness, queue lag, SVI diagnostics, fit quality, and dashboard alerts.

Series 05

A Derivasys engineering article on turning a BTC options volatility surface into a Kafka, Kubernetes, and Rust-ready worker pipeline.

FAQ

Derivasys is a live BTC and crypto options analytics dashboard for BTC, ETH, and altcoin volatility surfaces, SVI smiles, risk reversals, flies, fixed-tenor slices, and calibration diagnostics.

It is built for traders, quants, risk teams, and builders who need fast visibility into crypto options implied volatility and surface quality.

SVI stands for Stochastic Volatility Inspired. It is a compact parameterization used to fit implied total variance across option strikes and expiries.

Yes. WebSocket and REST API access can be made available to approved testers by email.

Use the live dashboard for surfaces, smiles, risk nodes, and diagnostics. Contact us for approved API access.